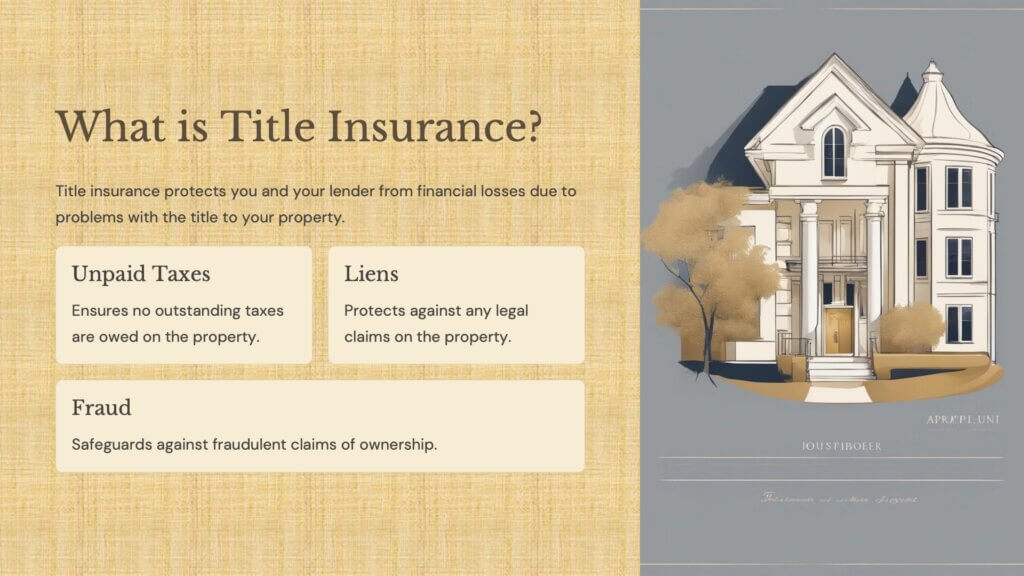

So, what exactly is title insurance? When you buy a home, title insurance protects you and your lender from financial losses due to problems with the title to your property—like unpaid taxes, liens, or fraud. It’s a crucial safeguard, ensuring that no one else can claim ownership of your home after you’ve bought it. However, the irony is that title issues are rare, especially in today’s world of digitized land records. Despite this, title insurance is still required by most lenders.

Leave a comment

Sign in to post your comment or sign-up if you don't have any account.